Pension sharing isn’t typically the first item that separating couples consider. Most people are concerned about what will happen to the family home. However, pensions are a significant asset and an important consideration when planning your future, so deciding what to do with them is critical. Sharing, offsetting, and earmarking are three possibilities for allocating pensions as part of a divorce settlement.

This article will focus on the pension sharing order in particular. It’s a terrific alternative for many people because you can make a clean separation from your ex-partner. We’ll look at the costs, process, annex, and timetable for the pension-sharing order following a divorce.

What is a Pension Sharing Order?

A pension sharing order is a mechanism used by the Court to allow a couple to separate their pensions during divorce proceedings or the dissolution of a civil partnership.

One of the most difficult tasks in a divorce is separating the financial assets you have as a couple, such as personal pensions, property, investments, and money.

When it comes to settling on a financial settlement and filing for divorce, your or your partner’s personal pension is likely to be the most valuable asset you own, after the family home.

Prior to the implementation of pension sharing in December 2000, a spouse who had not worked during their marriage could be left with no pension entitlement after a divorce.

However, with regard to pension sharing on divorce, the new method permits a couple divorcing or dissolving a civil partnership to issue a clean break order, distributing any pensions between them, or generating a new personal pension for the other spouse.

Following a divorce, pensions are separated between spouses by getting a consent order, which is a formal contract recognised by a Judge.

Related: FINAL SALARY PENSION TRANSFER: How It Works, Benefits and Risks

Pension Sharing Order Annex

Paperwork called a Pension Sharing Annex must be filed as part of the pension sharing order process. Following a divorce, this is merely the official document that allows an individual to get a portion of their spouse’s pension.

The pension sharing annexe directs the trustees of a pension system to pass or transfer a “pension credit” from the scheme member to the spouse. However, the pension trustees cannot execute the annex unless it is sealed by the courts and accompanied by a sealed Decree Absolute.

How Does a Pension Sharing Order Work?

The assets of a marriage or civil partnership are assessed within a pension-sharing order as part of the pension and divorce or dissolution process so that they can be divided between the couple.

Pensions are now included in the total value of marital assets as a result of divorce pension sharing.

It allows one person to receive a percentage of the total value of another person’s pension.

This money is known as pension credit, and it can be moved into a current pension, a new private pension, or an additional pension as part of the existing system.

When is Pension Sharing a Good Idea?

Pension pooling may be a good choice for you if you meet the following criteria:

In comparison to the other assets, one party has high-value pensions.

You’re nearing retirement age and will find it difficult to accumulate comparable pension benefits in a short period.

You intend to remarry soon, as the pension sharing order cannot be changed at a later date.

The divorced couple is in their forties. Under present laws, you can begin receiving pension credit benefits at the age of 50, rather than waiting until your ex retires.

You’d like to be allowed to name prospective beneficiaries of any death benefits if you die before receiving retirement benefits.

Overall, it promotes a clean break and gives the separating couple more flexibility and choice. The presence of the courts also aids in ensuring a fair distribution of marital assets.

However, if keeping the family home is a top priority for you, pension sharing might not be the best option. Pension sharing may necessitate the sharing of other assets, including the home, which may necessitate its sale. Furthermore, it may not be the first choice for individuals who already have a sufficient pension. If you are unsure what to do, please contact us to discuss your needs.

Pension Sharing Order Timescale

Determining the value of your pension

The court will consider whatever pensions you or your spouse may have.

This includes governmental pensions, employer-sponsored plans, and private pension plans.

Before you can set up pension sharing, you must first determine the value of any pensions you own. Include any of the following:

#1. Pensions provided by your employer

Additional State Pension (any pension from the State Pension system that is in addition to your basic State Pension, i.e. earned while working). (The basic State Pension cannot currently be split in a pension-sharing scheme.)

#2. Personal pension plans

The individual who holds the pension must apply for a pension valuation.

#3. Workplace pensions.

Workplace pensions might be a ‘defined contribution,’ which means you contribute a predetermined amount into a pension account.

In this scenario, consult your yearly statement, which will provide you with a ‘transfer value’ for your pension.

If, on the other hand, you have a final salary pension system that is based on your earnings, you may need to visit a financial consultant for a valuation.

This is because your computation will be more difficult, depending on how long you have contributed to the pension and how much you are paid.

Public-sector pensions can be more involved, therefore, we recommend speaking with the scheme first to receive the CETV and a summary of benefits.

To give these valuations, all schemes will collect fees, which might be extremely substantial.

Personal Pensions and Their Value

To determine the worth of a personal pension, consult your most recent annual statement.

This will determine the value of your pension and provide you with a ‘transfer value,’ which will be used by the court to determine your pension share.

Applying for Pension Sharing Orders

You must apply to a court for a pension-sharing order as part of your divorce to agree on a division of the pension pool.

Following an assessment of your marital assets, the court will give a proportion of one person’s pension worth to the other party, which is then used to establish a separate pension.

This separate pension could be an existing pension system or a new pension scheme.

It is recommended to consult with an independent financial adviser about the best manner to distribute the pension credit.

The pension trustees will also charge you for implementing the pension sharing order, which is expensive.

Before proceeding, please find out the costs of the pension sharing order and consider sharing the charges between you.

Is it Possible to Share State Pensions?

Even though the basic State Pension is not included, you may be able to claim one through your ex-national partner’s insurance.

This would solely apply to the years you spent together as a couple and would have no bearing on their individual State Pension.

If you remarry (or get into another civil partnership) before reaching the official State Pension age, you will forfeit this right.

Costs of a Pension Sharing Order

Is it less expensive to place a pension-sharing order online? Many people are concerned about the costs of pension-sharing orders in a divorce, with high street solicitors charging £200 per hour to create the documentation and negotiate with the pension company.

The order is part of what is known as a financial consent order, which also addresses all other parts of your marriage finances, such as property, assets, and finances.

How Long Does it Take to Obtain a Pension Sharing Order?

It typically takes six to nine months to complete the legal process of separating and have the court accept your consent order. This schedule is based on data from Amicable; if you pursue another path, such as a court, it could take much longer.

It is crucial to note that some pension providers can take a long time to provide the numbers you will need to present to the court when applying for a consent order, so make sure to seek your pension CEVs as soon as possible.

What happens after a Pension Sharing Order is Issued?

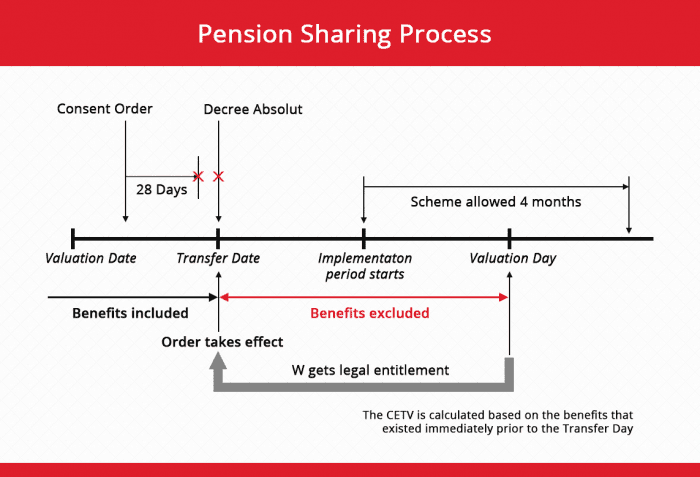

The pension debit/credit does not occur immediately once the court has approved your consent order and made your pension sharing order. The pension sharing order becomes legally obligatory, or “takes effect,” on the later of the following two dates:

- the date of the absolute edict or

- 28 days from the date the pension sharing order was issued (7 days after the time given to appeal the order, runs out)

Keep in mind that if you petition for a decree immediately following the consent order, your divorce will be finalised before the pension sharing order takes effect. This can put the intended recipient in a dangerous situation. If the pension holder died before the 28 days was up, the beneficiary could be out of pocket. They would no longer be eligible for substantial spousal death benefits under the pension because they were no longer the deceased’s spouse.

They would also be denied the pension credit because the pension sharing order would never be implemented. As a result, it is preferable to wait at least 28 days from the date of the pension sharing order before asking for your decree absolute (some financial remedy orders state this, in which case you must wait). The pension sharing order will subsequently go into effect once the decree absolute is issued.

How quickly will the Pension Provider(s) put the Pension Sharing Order into Effect?

As soon as you receive the Decree Absolute from the court, you can send all appropriate papers to the pension provider(s) and request that the pension sharing order be implemented. You must send them the following documents:

- The court-stamped initial consent order,

- The original pension sharing annex (Form P1) stamped by the court,

- a copy of the absolute decree,

- a certified copy of the decree nisi

- Payment of their fees (if there are any)

- If it is an external transfer, the information about the new pension system will get the pension credit.

The pension provider then has four months from the day the paperwork is received to implement the directive.

Is it Possible to Share a Pension after a Divorce in Another Country?

A foreign court lacks jurisdiction to make a pension-sharing order against a UK pension arrangement. If a couple divorces outside of the UK and wishes to share the benefits held under a UK pension scheme, they must get a pension-sharing order from a UK court. The relevant court order would be made under Part III of the Matrimonial and Family Proceedings Act 1984 (or the equivalent Scottish legislation) and would need to follow the usual format of a UK court order, quoting the UK plan number and the relevant percentage or amount (Scotland only) to be shared.

If the ex-spouse or ex-civil partner is residing in another country at the time of the divorce and does not already have a UK pension arrangement, they may have problems setting one up to receive their pension credit. Another possibility is to transfer the pension credit directly to a qualifying recognized overseas pension scheme (QROPS).

What are the Formal Documents Required for Pension Sharing?

A pension-sharing order must be issued by the court in England and Wales, and it must be accompanied by a prescribed pension-sharing order annex (Form P1) for each pension arrangement that is to be shared. An annex should include the name of the provider, the reference number of the pension arrangement being shared, and the percentage of the arrangement that the ex-spouse or ex-civil partner will receive.

In Scotland, pension sharing can be accomplished through either a court-ordered pension sharing order or a similar clause in a ‘qualifying agreement.’ A qualifying agreement (the more common method) is a written financial agreement between the two parties, usually drafted by their legal counsel, that is recorded in a government register called the ‘Books of Council and Session.’ An annex to both an order and an agreement should include the provider’s name, the reference number of the pension arrangement being shared, and the percentage of the arrangement or the cash amount from the arrangement that the ex-spouse or ex-civil partner is to receive.

The date the share is to be made should not be quoted in an order or agreement because this date is chosen by the scheme administrator/trustees of the member’s scheme. It should be noted that the pension sharing annex in England and Wales must state the amount to be split as a percentage. The annex in Scotland might display a percentage or a monetary sum.

What happens if a mistake is made during the Pension Sharing Process?

Sometimes things go wrong, and pension sharing may not work out as planned. For example, you may have received a lot smaller sum than you anticipated. Perhaps you believe your spouse forgot to report all of their pension assets. Do not be alarmed; there are several options for dealing with these problems.

If you believe your solicitor has failed to effectively represent your pension rights through a divorce, you should speak with them. They may be able to solve the problem, and if it was caused by their error, you may not be charged.

If your solicitors failed to properly represent your claims during the pension sharing procedure and you are unable to repair the problem, you may be entitled to sue them for negligence. You may be able to obtain compensation if you take your complaint to court.

What Effect does Pension Sharing have on My Lifetime Allowance?

As you may be aware, there is a limit to the amount you can have in your pension fund. Over this limit, you will be unable to take advantage of the different tax benefits offered by pension systems. This is referred to as the Lifetime Allowance.

Until 2009, you could request a higher Lifetime Allowance to ensure that the division of pensions upon divorce did not drive you over the limit. However, this is no longer the case. For the Lifetime Allowance, whatever pension credit you obtain is added to the rest of your retirement funds. A pension-sharing order does not provide tax relief.

At the same time, transferring a pension debit to your ex-partner diminishes the value of your pension pile. As a result, you may have more of your Lifetime Allowance available after your divorce.

Is a Pension Sharing Order a Factor in Determining One’s Retirement Age?

The easy answer to this question is no. Following a divorce, one’s pension age remains the same. One cannot begin taking pension benefits just because they profited from a transfer.

Pension Sharing Order FAQ’s

What is the difference between a pension sharing order and a pension attachment order?

A pension sharing order divides the parties’ pension provision at the time of divorce and leaves the parties with separate pension funds, whereas a pension attachment order is a sort of maintenance order that requires the pension system to pay a set percentage of the monthly pension payments.

Who pays for a pension sharing order?

If you cannot agree on who will pay, the charges are borne by the pension owner (the person sharing the pension).

Can a pension sharing order be Cancelled?

A Pension Sharing Order can sometimes be overturned, but only with a Court’ Variation Order, and there are stringent time constraints. When a decree absolute is given, it is usually impossible to change an Order. You should contact your Solicitor as soon as possible to see if a Variation Order is possible.